Last updated on January 9th, 2026 at 06:07 am

Filing “Single” when you’re legally married is considered an incorrect filing status by the IRS ,and it can lead to back taxes, interest, and even penalties if left uncorrected.

While it’s true that there’s no penalty for choosing Married Filing Separately (a legitimate status), claiming “Single” when you’re still legally married is viewed as a false filing, even if it was an honest mistake. Many taxpayers make this error after seeing general advice online or assuming that living apart makes them “single” in the eyes of the IRS. The reality is that your marital status as of December 31 determines how you must file.

At J. David Tax Law, we’ve seen how quickly a simple oversight like this can turn into an IRS notice, a tax balance, or a full-blown enforcement case, but it’s fixable with the right legal guidance.

The Common Confusion: Filing Separately vs. Filing Single

Many taxpayers are surprised to learn that “filing separately” and “filing single” are not interchangeable terms. In fact, misunderstanding the difference is one of the most common filing mistakes the IRS sees each year.

Filing Separately (Married Filing Separately Status)

Married Filing Separately (MFS) is a legitimate IRS filing status for married taxpayers who prefer to report income, deductions, and credits individually rather than jointly. It’s often used when:

- One spouse owes federal or state tax debt, and the other wants to protect their refund.

- A spouse has large medical or miscellaneous deductions that would be limited on a joint return.

- There are privacy or legal concerns, such as pending divorce or separate finances.

When used correctly, filing separately can legally limit your liability to your own income and taxes — a strategic choice if your spouse’s finances or filings could put you at risk. However, it usually results in higher combined tax liability and limits key tax credits, which we’ll cover later.

Filing Single (When You’re Actually Married)

Filing Single when you are legally married is not allowed under IRS law unless you are legally separated or divorced according to your state’s statutes. The IRS determines your filing status based on your marital status as of December 31 of the tax year. So even if you and your spouse lived apart all year, you are still considered married unless a court has formally ended or legally separated the marriage.

Choosing “Single” while still married can lead to serious issues:

- The IRS may disallow your return and recalculate your taxes under the correct status.

- You could lose credits and deductions claimed under “Single.”

- You may owe additional tax, interest, or even accuracy-related penalties.

- In cases of deliberate misfiling, the IRS could pursue fraud charges under IRC § 7206 or § 7201.

In short, Married Filing Separately is legal but restrictive; filing Single while married is a filing error that can trigger IRS correction or enforcement.

While Married Filing Separately is a legitimate filing option, it typically results in fewer tax benefits and higher combined liability. J. David Tax Law can help you determine whether this approach is strategically beneficial — especially if you already owe or are under IRS review.

What Are the 5 IRS Filing Statuses?

To understand why filing “Single” while married is a mistake, it helps to start with the basics. The IRS recognizes only five official filing statuses, each tied to your marital and family situation as of December 31 of the tax year. Your filing status determines your tax rate, standard deduction, and eligibility for specific credits and deductions.

Below is a clear comparison showing how each status works and who qualifies:

Filing Status | Who It Applies To | Key Details |

Single | Individuals who are unmarried or legally separated under state law | Simplest status; standard deduction of $14,600 (for 2024); not available if still legally married |

Married Filing Jointly (MFJ) | Married couples filing one combined return | Usually the most tax-advantageous option; both spouses share income, deductions, and tax liability |

Married Filing Separately (MFS) | Married taxpayers choosing to file individually | Legal option; limits credits like EITC and education credits but can protect one spouse from the other’s tax debt |

Head of Household (HOH) | Unmarried or “considered unmarried” taxpayers who pay over half the cost of maintaining a home for a qualifying dependent | Offers higher deduction and better tax brackets than Single; strict dependency requirements apply |

Qualifying Widow(er) | A taxpayer whose spouse died in the past 2 years and who has a dependent child | Allows use of joint-return rates for up to two years after the spouse’s death |

When Does Married Filing Separately Make Sense?

While it’s true that most couples save more by filing jointly, there are specific situations where filing separately can be a strategic legal or financial move, especially if one spouse faces IRS issues or financial risk.

Here are a few common reasons why married taxpayers might choose to file separately:

Protecting Yourself From Your Spouse’s Tax Debt

If one spouse owes back taxes, has unfiled returns, or is under IRS enforcement, filing separately can help protect the other spouse’s refund and prevent joint liability. Each filer is only responsible for their own reported income and taxes.

High Medical or Miscellaneous Deductions

Because medical and certain other deductions are limited by a percentage of your Adjusted Gross Income (AGI), a spouse with significant out-of-pocket medical expenses might qualify for more deductions if they file separately.

Privacy or Legal Separation

In cases of divorce proceedings, financial disputes, or simply wanting to keep income private, filing separately may make sense until your marital or legal situation is finalized.

State and Community-property Law Considerations

In community-property states (like California, Texas, and Arizona), income and deductions are divided evenly between spouses. Filing separately can sometimes create a clearer separation of liability, especially if only one spouse has tax exposure.

If you’re unsure whether to file jointly, separately, or if you’ve already chosen the wrong status, call us at (888) 342-9436. Our experienced tax attorneys can review your situation, explain your legal options, and help you file or amend correctly to avoid unnecessary IRS penalties or debt.

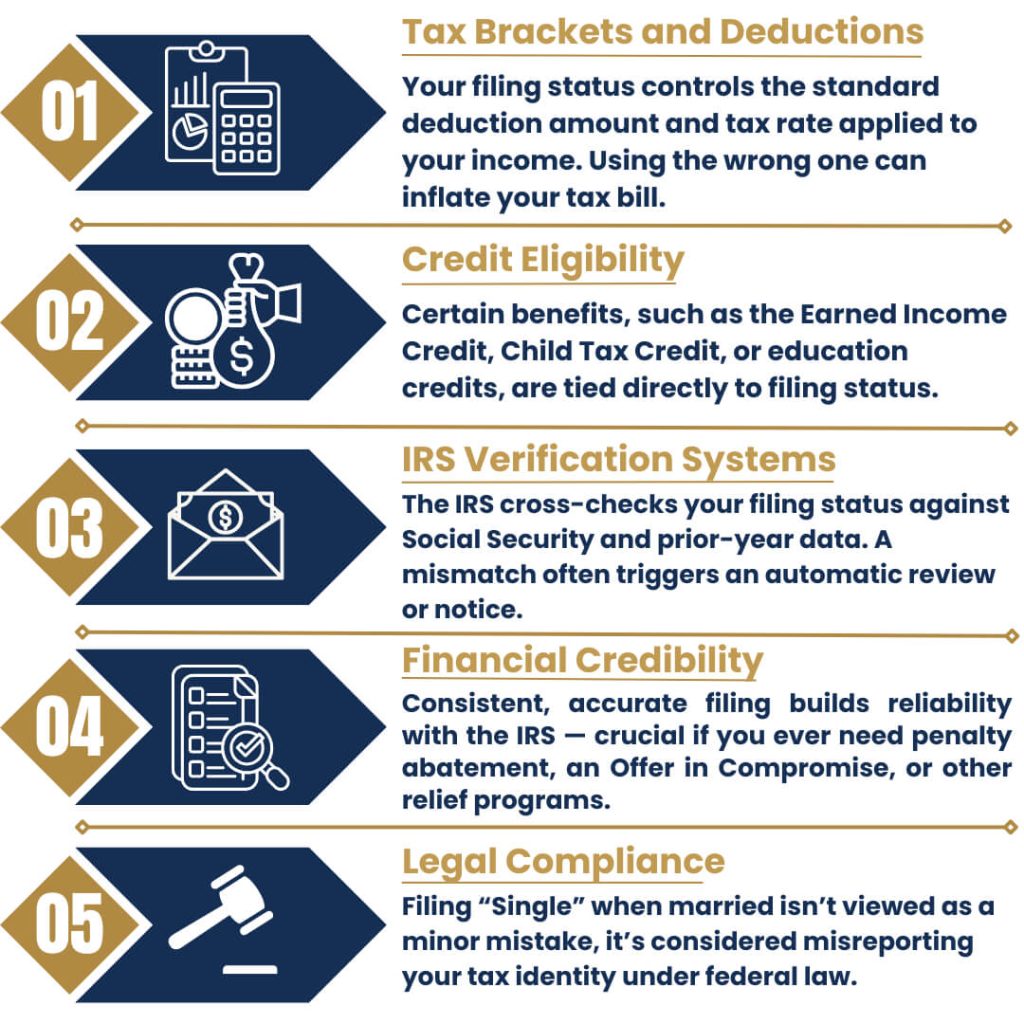

Why Correct Filing Status Matters

Choosing the right filing status affects far more than just your tax bracket. It determines your eligibility for deductions, credits, and how the IRS reviews your return. Selecting the wrong status—especially filing “Single” while married—can quickly lead to corrections, penalties, or even audit reviews.

Here’s why accuracy matters:

Risks & Penalties of Filing Single While Married

Here’s what can happen if you file “Single” while married:

Additional Taxes and Interest

The IRS will adjust your return to the correct status, often resulting in a higher tax bill and interest charges on any unpaid balance.

Loss of Credits and Deductions

You may lose credits such as the Earned Income Tax Credit, Child Tax Credit, or education-related deductions that were claimed under the wrong status.

Accuracy-Related Penalties (Up to 20%)

If the IRS determines that your incorrect filing caused an underpayment, it can impose a 20% penalty on the amount owed under IRC §6662.

Potential Fraud or False Statement Charges

In rare cases where the IRS believes the misfiling was intentional, it can be treated as tax fraud under IRC §7206 or tax evasion under §7201, which carry fines up to $250,000 and potential criminal liability.

Audit and Enforcement Risk

Mismatched filing statuses—such as one spouse filing “Single” while the other files “Married”—are automatically flagged by IRS systems and can trigger an audit or further investigation.

If you’ve already received an IRS notice or suspect your filing was incorrect, contact J. David Tax Law at www.jdavidtaxlaw.com/. Our attorneys can help correct your return, negotiate penalty relief, and protect you from further enforcement action.

Innocent Spouse and Liability Relief Options

If your spouse filed incorrectly or selected the wrong status without your knowledge, you may not have to share the consequences. The IRS offers several forms of relief that can remove or reduce your responsibility for taxes, interest, or penalties tied to a joint or misfiled return.

The most common option is Innocent Spouse Relief, which applies when your spouse made an error or omission on a return and you had no reason to know about it. If granted, the IRS will separate your liability and prevent further collection against you for those debts. Read more about the four types of Innocent Spouse Relief here.

Get Help

If you filed Single or Separately while married and aren’t sure it was correct, the safest move is to get legal guidance before the IRS acts. A wrong filing status can lead to penalties, back taxes, and lost credits, but it can be corrected with help from a tax attorney. Contact us to review your return, fix filing errors, and protect yourself from future IRS enforcement.

Frequently Asked Questions

Filing Single while legally married is not allowed under IRS rules unless you are legally separated or divorced. The IRS may correct your return, assess back taxes, add penalties, and disqualify you from certain credits.

You can file Married Filing Separately (MFS) if you’re legally married but choose to file your own tax return. Each spouse reports their own income, deductions, and credits. However, many credits — such as the Earned Income Credit and education credits — are not available when filing separately.

You must use Married Filing Separately if you and your spouse choose not to file a joint return, or if one spouse refuses to sign a joint return. It’s also used when one spouse has significant tax debt, or when separating legal and financial responsibility is necessary.

For the 2025 tax year, the standard deduction for Married Filing Separately is $15,750, the same as the Single filing status.

There is no IRS penalty for using the Married Filing Separately status — it’s a legitimate filing option. However, it often results in a higher combined tax bill and fewer available credits compared to filing jointly.