When the IRS adds penalties and daily compounding interest to your balance, time becomes your most expensive mistake. This free IRS penalty and interest calculator lets you see, in seconds, how much your back taxes, late filing penalties, and IRS late payment penalties have grown. Built around official IRS computation methods, it gives taxpayers clarity before facing enforcement actions such as levies or wage garnishments.

At J. David Tax Law, every number matters because every number represents a risk — to your income, assets, and peace of mind. Our team uses the same data-driven approach behind the IRS penalty calculator to help clients legally reduce or eliminate penalties through proven resolution strategies.

Use our IRS Penalty and Interest Calculator now to get a true-to-life estimate before penalties compound again.

Not Sure How Much You Owe?

Why the IRS Adds Penalties and Interest to Your Tax Debt

The IRS doesn’t just charge you for unpaid taxes — it charges you for time. Every day you delay payment, the balance compounds through a combination of failure-to-file penalties, late payment penalties, and interest that grows until your account is settled.

Types of IRS Penalties You Could Face

Each penalty serves a specific enforcement purpose. Understanding which applies to you helps you interpret your results from the IRS Penalty and Interest Calculator.

-

Failure-to-File Penalty

Charged when you don’t submit your return by the due date (usually April 15).

Maximum: 5% per month (up to 25%). -

Failure-to-Pay Penalty

Added when you file but don’t pay the full balance owed.

Maximum: 0.5% per month (up to 25%). -

Accuracy-Related Penalty

Applies if you underreport income or make substantial errors.

Maximum: 20% of the underpaid tax. -

Fraud Penalty

Assessed for intentional evasion or falsified returns.

Maximum: Up to 75% of the unpaid tax.

Together, these penalties can push your total balance to nearly 47.5% more than the original tax owed before interest even begins to accumulate. That’s why using a tax penalty calculator or IRS late payment calculator early can prevent massive compounding costs later.

Read more

Other IRS Penalties You May Encounter

The IRS also issues notices and letters for several additional penalties that aren’t always visible on your first bill. These include:

-

Information return penalty – For not filing or furnishing required information returns (like 1099s or W-2s) accurately or on time.

-

Erroneous claim for refund or credit penalty – For submitting an excessive or false refund claim without reasonable cause.

-

Failure to deposit penalty – For not paying employment taxes accurately or on schedule.

-

Tax preparer penalties – For preparers who submit false or negligent returns.

-

Underpayment of estimated tax (corporations) – For not making timely, accurate estimated payments at the corporate level.

-

Underpayment of estimated tax (individuals) – For individuals who underpay quarterly estimated taxes.

-

International information reporting penalty – For failing to timely and correctly report foreign financial accounts or assets.

Each of these can trigger IRS notices, such as CP2000, CP14, or Letter 5005, and they often include overlapping interest charges. Use the free IRS penalty and interest calculator to see how these penalties and daily-compounding interest could affect your total balance.

How Do You Know if You Owe a Penalty to the IRS?

Most people first find out through an IRS notice, but the agency doesn’t always specify how each amount is calculated. To verify, you can:

-

Review letters such as CP14, CP501, or CP503.

-

Log in to your IRS Online Account to see your penalty breakdown.

-

Use the IRS late payment penalty calculator to estimate the total amount owed with interest.

If you’ve ignored returns for multiple years, you may already be facing penalties for not filing taxes for 5 years — one of the costliest mistakes taxpayers make. A tax attorney can help you analyze these notices and explore your legal options for penalty relief.

Does the IRS Charge Interest on Penalties?

Yes, and this is where many taxpayers are caught off guard. The IRS applies daily-compounding interest not only to unpaid taxes but also to the penalties themselves. The rate changes quarterly under IRC §6621, typically the federal short-term rate + 3%.

Think of it like a high-interest loan that renews every 24 hours. A tax interest calculator can show how a $10,000 balance can grow by hundreds within a few months.

⚖️ Pro Tip: The IRS treats penalties and interest as separate components of debt — meaning even if you reduce one, the other continues to build. Before entering any payment plan, confirm your total liability using the IRS Penalty and Interest Calculator.

How Our IRS Penalty and Interest Calculator Works

This Penalty and Interest Calculator is designed to give taxpayers a realistic picture of their total IRS liability, including late filing, late payment, and daily-compounding interest. Unlike generic tools, it uses official IRS formulas to mirror how penalties actually accrue, helping you make informed financial and legal decisions before the situation escalates.

Step-by-Step: How to Use the Calculator

Using the IRS penalty and interest calculator is simple. You don’t need your entire tax transcript, just the essential information the IRS uses to calculate penalties and interest.

1. Select Your Tax Year

2. Choose Taxpayer Type

3. Enter the Original Tax Due

4. Add Key Dates

5. Click “Calculate”

The tool automatically computes the total estimated penalties and interest — displaying a breakdown for failure-to-file, failure-to-pay, and interest on both.

Example:

If you owed $12,000 for tax year 2021 and filed your return eight months late, the late filing penalty calculator will show approximately $1,200 in penalties plus daily interest that continues until full payment.

What Makes This Calculator Accurate

The IRS penalty calculator follows the same logic outlined in IRS Publication 17 and Topic No. 653 – IRS Penalties. It applies:

Daily Compounding Interest: Based on quarterly IRC §6621 rates.

Per-Month Penalty Accrual: For both filing and payment delays.

Automatic Cap Recognition: Penalties stop increasing once maximum limits are reached.

These calculations ensure that the tax penalty calculator reflects real IRS math — not approximations — and can be trusted to plan your next steps.

What the Calculator Doesn’t Include

No online tool can perfectly predict your IRS balance because several factors depend on your specific case:

Unassessed penalties from audits or new IRS notices

Payments or credits not yet applied to your account

State-level penalties (these vary by jurisdiction)

Interest adjustments on amended returns or appeals

That’s why J. David Tax Law always recommends reviewing your calculator results with an experienced tax attorney who can interpret the data and identify penalty abatement or Offer in Compromise options.

Realistic Example Using the Calculator

Let’s say you owed $20,000 in taxes for 2022 but didn’t file or pay until July 2024. Here’s how the calculator breaks that down:

| Penalty Type | IRS Rule Applied | Estimated Amount |

|---|---|---|

| Failure-to-File Penalty | 5% per month, capped at 25% | $5,000 |

| Failure-to-Pay Penalty | 0.5% per month, capped at 25% | $2,000 |

| Interest on Tax + Penalties | Daily compounding, quarterly §6621 rate | ≈ $1,100 |

| Total Estimated Balance | $28,100 |

Result: You now owe roughly $8,100 more than your original balance — and the meter is still running.

What to Do After Using the Calculator

Once you’ve used the Penalty and Interest Calculator, you now have what most taxpayers don’t — visibility. That number on your screen isn’t just a total; it’s a map of how far your tax debt has grown and how much it can still increase if you wait.

The next step is to act before the IRS does. Depending on what your IRS penalty calculator shows, here’s how to move from estimate to resolution.

1. If Your Balance Is Recent (Under 12 Months)

Apply for First-Time Penalty Abatement (FTA). This program can remove failure-to-file or failure-to-pay penalties for taxpayers with a clean compliance record.

You may qualify if:

- You’ve filed all required returns (or valid extensions).

- You’ve paid or arranged to pay your taxes.

- You haven’t had prior penalties in the past three years.

2. If Your Penalties Seem Excessive

You may be eligible for Penalty Abatement for Reasonable Cause. The IRS grants this relief when circumstances beyond your control prevented timely filing or payment.

Common qualifying reasons include:

- Medical emergencies or family illness

- Natural disasters or business closures

- Reliance on incorrect IRS advice

- Serious financial hardship

An attorney can file for abatement using Form 843, requesting full or partial removal of penalties.

3. If the Balance Feels Unmanageable

There are still structured legal solutions:

- Offer in Compromise — Settle your debt for less than the full amount.

- Installment Agreement — Make affordable monthly payments.

- Currently Not Collectible — Pause collections due to financial hardship.

4. When to Call a Tax Attorney

If your estimate includes multiple years of debt or penalties for not filing taxes for 5+ years, professional intervention is essential. The IRS will typically begin enforcement actions such as:

A J. David Tax Law attorney can:

- File immediate legal requests to halt enforcement

- Negotiate penalty relief or settlement terms

- Represent you in direct communication with IRS collections

Case Example: How J. David Tax Law Removed $150,888 in Penalties and Interest

A Louisiana taxpayer reached out after their state tax balance had grown to $330,429, including $92,604 in penalties and $58,284 in interest, added to a $179,541 principal balance for tax year 2010. J. David Tax Law successfully removed $150,888 in penalties and interest and negotiated a structured resolution.

What we found

-

The taxpayer had fully paid the $179,541 principal in July 2016, but the state continued to assess penalties and daily compounding interest.

-

Multiple prior requests for penalty and interest waivers had been rejected despite the client’s eligibility under state rules.

Payment application errors and procedural oversights by the Louisiana Department of Revenue had prevented the client’s relief request from being properly reviewed.

Our Legal Strategy

-

Submitted formal Penalty and Interest Waiver Requests citing the state’s reasonable cause provisions and referencing prior compliance history.

-

When the state denied relief three separate times, Ryan, the lead attorney on the case, escalated the matter by identifying discrepancies in how payments had been applied to the taxpayer’s account.

Contacted a supervising Revenue Officer directly, presented documentation showing proper payment allocation, and requested supervisory review of the previous denials.

The Outcome

Following a thorough reexamination of the file, the Louisiana Department of Revenue approved a full waiver of all penalties and interest, removing $150,888 from the client’s account.

The approval not only eliminated the assessed penalties and interest but also closed the client’s case as fully resolved — with a zero balance on all non-principal charges.

⚖️ Result: Total savings of $150,888, achieved after three prior rejections through persistent advocacy and procedural precision. The client avoided enforced collection and achieved complete relief on all non-tax portions of their debt.

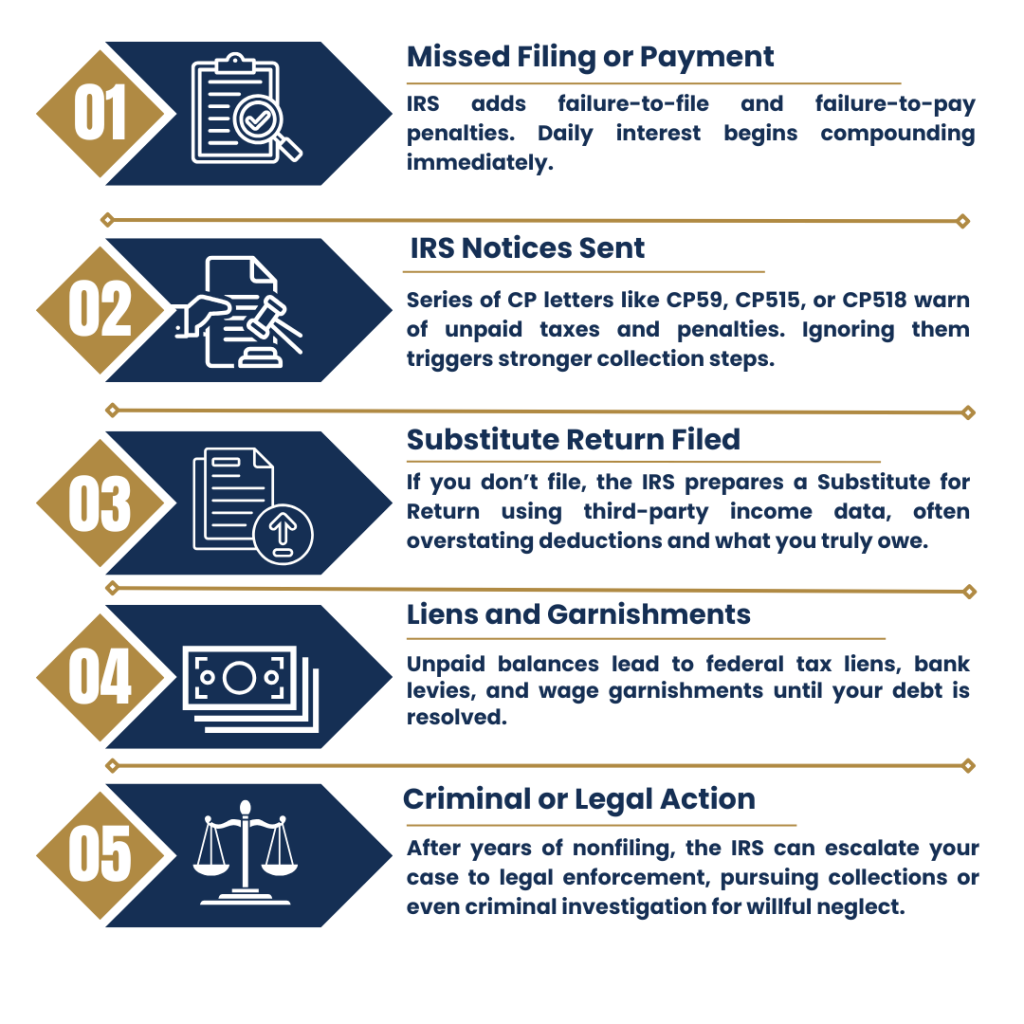

What Happens When You Don’t File Taxes for Years

Common Mistakes When Estimating IRS Penalties

Even with the best tools, many taxpayers underestimate how fast penalties and interest grow. Using a tax penalty calculator gives you a powerful estimate, but only if the inputs are accurate. Here are the most common errors that can lead to misleading or inflated totals.

1. Using the Wrong Filing or Payment Dates

The most frequent mistake is entering the wrong return due date or actual filing date.

- Filing extensions shift due dates but don’t pause failure-to-pay penalties.

- Entering the standard “April 15” instead of your extended due date can change your estimate by thousands.

2. Ignoring Partial Payments or Credits

If you’ve made any estimated payments, withholdings, or previous installment payments, they must be included.

- Many taxpayers use a free IRS penalty and interest calculator and forget to account for prior credits.

- That omission can exaggerate what you owe and trigger unnecessary fear or missed relief opportunities.

3. Confusing IRS and State-Level Penalties

Federal and state tax agencies apply penalties differently.

- The IRS penalty calculator uses federal compounding rules under IRC §6621, while states like California, New York, and Florida use their own penalty rates and structures.

- Always confirm whether your total is from the IRS or your state before planning repayment.

4. Overlooking Daily Compounding Interest

Interest doesn’t grow monthly — it compounds daily on both tax and penalty balances.

- Even a week of delay after running your IRS late payment calculator can change your total.

- Always recheck your calculation if you don’t act immediately.

5. Assuming Penalties Stop Once You File

Many taxpayers think filing the missing return ends penalties. In reality:

-

The failure-to-file penalty stops once you submit.

-

But the failure-to-pay penalty and interest continue until the balance is paid in full.

Use a tax interest calculator to project ongoing growth after you’ve already filed.

6. Not Verifying With a Tax Attorney

Online calculators provide helpful estimates, not legal guarantees. A J. David Tax Law attorney can confirm whether your penalties qualify for:

-

First-Time Abatement

-

Reasonable Cause Relief

-

Interest Reduction Requests

Get Help After Using the IRS Penalty and Interest Calculator

Calculating your penalties is only step one; resolving them correctly is where results happen. This calculator gives you a clear snapshot of what you owe, but only an attorney can help you reduce, remove, or legally settle those amounts.

At J. David Tax Law, every case is handled by an experienced tax attorney, not a call center or third-party consultant. Our team has successfully helped clients:

- Remove tens of thousands in penalties through Penalty Abatement.

- Stop wage garnishments and levies within 48 hours.

- Negotiate fair Installment Agreements and Offers in Compromise.

- Restore full compliance with the IRS and state tax agencies.

⚖️ Why It Matters: Waiting just 30 days after your first IRS notice can increase your balance significantly through daily compounding interest. Acting quickly gives your attorney more leverage and more relief options.

Don’t let IRS penalties grow another day! Call (888) 342-9436 to get an attorney’s insight before interest compounds further.

Frequently Asked Questions

You can calculate penalties and interest instantly using the IRS Penalty and Interest Calculator. Enter your tax year, amount owed, filing date, and payment date. The tool applies official IRS formulas to estimate failure-to-file, failure-to-pay, and daily-compounding interest charges — showing your total balance in seconds.

Yes — interest applies to both unpaid tax and the penalties themselves. This means even if your penalties reach their maximum cap, interest continues to grow daily until your balance is paid or resolved through legal relief.

Checking your estimate regularly with the IRS penalty calculator helps track this growth accurately.