You can avoid paying taxes on debt settlement only if you qualify for an IRS exclusion and report it correctly. In most cases, forgiven debt is treated as taxable income, but the IRS allows certain legal exceptions — most commonly the insolvency exclusion and the bankruptcy exclusion — that can remove some or all of the canceled debt from your taxable income.

To avoid paying taxes, you must meet the eligibility requirements at the time the debt is canceled and properly file the required IRS forms, such as Form 982, along with supporting documentation. If you do not qualify for an exclusion or fail to report the settlement correctly, the IRS will treat the forgiven amount as income and assess taxes, penalties, and interest.

Key Takeaways

- Forgiven or settled debt is generally treated as taxable income unless a specific IRS exclusion applies.

- The most common ways to avoid paying taxes on debt settlement are qualifying for the insolvency exclusion or having the debt discharged through bankruptcy.

- Insolvency and bankruptcy must exist at the time the debt is canceled, not afterward.

- Even when an exclusion applies, forgiven debt must be reported correctly, often using IRS Form 982.

- Receiving Form 1099-C does not automatically mean you owe taxes, but it does mean the IRS expects the debt to be addressed on your return.

- Errors or omissions in reporting can lead to IRS notices, penalties, interest, and collection actions.

- Planning, documentation, and proper filing are what determine whether debt settlement results in tax relief or new IRS problems.

What Is Debt Settlement?

Debt settlement is a process in which a creditor agrees to accept less than the total amount you owe as full payment of a debt. This is most common with unsecured debts such as credit cards, personal loans, medical bills, and some types of business debt. Creditors may agree to a settlement when an account is delinquent or charged off, allowing them to recover a portion of the balance rather than risk receiving nothing.

While debt settlement can reduce what you owe, it does not erase the financial impact entirely. From a tax standpoint, the portion of the debt that is forgiven is often treated as canceled debt, which can create tax consequences even though no money is paid directly to you.

Do You Have To Report Settled Debts?

In most cases, yes. The IRS generally requires taxpayers to report settled or forgiven debt as income. If a creditor cancels $600 or more of a debt, they will usually issue Form 1099-C, which reports the amount of canceled debt to both you and the IRS. Even if you do not receive a 1099-C, the canceled amount may still need to be reported on your tax return.

The IRS is Forgiving Millions Each Day. You Could Be Next.

Why Canceled Debt Is Taxable Under IRS Rules

When a creditor agrees to accept less than the full balance owed, the IRS does not view the forgiven amount as “free money.” Instead, it is treated as cancellation of debt income, often referred to as CODI. Under federal tax law, income is generally taxable unless a specific exclusion applies, and forgiven debt falls squarely under that rule. This is why debt settlement often creates significant tax implications, even though you do not receive cash from the settlement itself.

Understanding why the IRS taxes canceled debt is essential to understanding debt settlement tax implications, avoiding reporting mistakes, and determining whether you qualify for an exclusion that could reduce or eliminate the tax burden.

The IRS considers debt to be income when you are no longer legally required to repay it. From the IRS’s perspective, being released from a financial obligation improves your financial position in the same way earning income would. As a result, canceled debt is generally treated as taxable income unless an IRS exception applies.

The IRS may treat canceled debt as taxable income in situations such as:

- Credit card debt settlements

- Personal loan settlements

- Medical debt settlements

- Business debt settlements

- Certain types of loan forgiveness

These rules apply broadly to debt and taxes, which is why many taxpayers are surprised by the tax consequences of settling debt.

If a creditor cancels $600 or more of a debt, they are typically required to issue Form 1099-C, Cancellation of Debt. This form reports the amount of forgiven debt to both you and the IRS and is often what triggers concerns about paying taxes on debt settlement.

A creditor may issue a Form 1099-C when:

- $600 or more of a debt is canceled

- A settlement agreement forgives part of the balance

- A debt is discharged, abandoned, or deemed uncollectible

- The creditor is required to report the cancellation to the IRS

Receiving a 1099-C does not automatically mean you owe taxes on the forgiven amount. It does mean the IRS is aware of the canceled debt and expects it to be properly addressed on your tax return.

Strategies To Avoid Paying Taxes On Settled Debt

Avoiding taxes on settled debt requires more than negotiating a lower payoff. Under IRS rules, forgiven debt is often taxable, but there are legal strategies that may reduce or eliminate the tax burden when applied correctly. Understanding these strategies before or immediately after settlement is critical to avoiding unnecessary tax consequences and IRS enforcement actions.

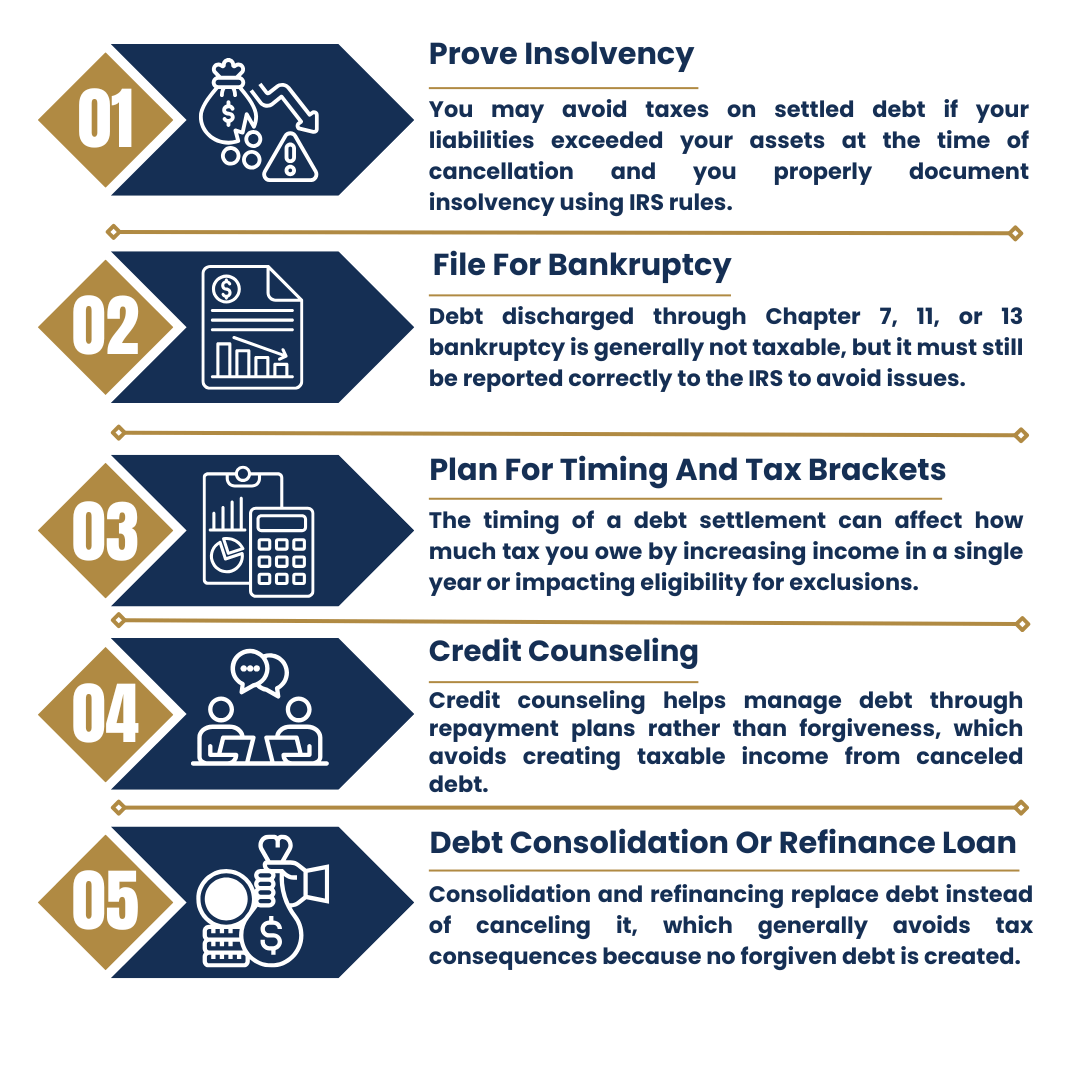

1. Prove Insolvency

The insolvency exclusion is the most commonly used method for avoiding taxes on debt settlement. If you were insolvent at the time the debt was forgiven, the IRS may allow you to exclude some or all of the canceled debt from taxable income.

What It Is And When It Applies To Business Owners

For IRS purposes, insolvency means that your total liabilities exceeded the fair market value of your assets immediately before the debt was canceled. This applies to both individuals and business owners, although the assets and liabilities considered may vary depending on business structure.

For business owners, insolvency may include:

- Business debts and personally guaranteed obligations

- Outstanding loans, credit lines, and merchant cash advances

- Business and personal assets when personal liability exists

If liabilities exceed assets, you may qualify to exclude forgiven debt up to the amount of your debt insolvency, making this one of the most effective ways to avoid paying taxes on debt settlement.

How To Document Insolvency For The IRS

Knowing how to prove insolvency to the IRS is essential. Insolvency must be calculated using documented values, not estimates or assumptions.

To properly document insolvency, taxpayers generally must:

- List all assets at fair market value

- List all liabilities owed immediately before cancellation

- Calculate the difference between assets and liabilities

- Complete the IRS insolvency worksheet found in Publication 4681

Attach IRS tax form 982 to the federal tax return

2. File For Bankruptcy

Filing for bankruptcy is another IRS-recognized way to avoid paying taxes on debt settlement when debt is legally discharged through the court system. When a debt is canceled as part of a bankruptcy case, the IRS generally does not treat the forgiven amount as taxable income. This exclusion can significantly reduce the tax implications of debt relief, especially in situations involving large balances or business obligations.

Unlike other strategies, bankruptcy removes the tax issue at its source by eliminating the debt under federal law rather than relying on financial conditions alone.

When debt is discharged through a Title 11 bankruptcy case, including Chapter 7, Chapter 11, or Chapter 13, the IRS excludes that debt from cancellation of debt income. This applies to both personal and business debt, provided the cancellation occurs as part of the bankruptcy proceeding.

For business owners, this can eliminate the tax on debt forgiveness that would normally apply after a settlement. Business debt that is discharged through bankruptcy is not treated as taxable income, even when a creditor issues a Form 1099-C. In these cases, the bankruptcy exclusion takes priority under IRS rules.

Even though bankruptcy eliminates the taxability of discharged debt, it must still be reported correctly on your tax return. Taxpayers typically must:

- Complete IRS tax form 982

- Indicate that the debt was discharged through bankruptcy

- Attach the form to the federal tax return for the year the debt was canceled

Failing to report the bankruptcy exclusion properly can lead to IRS notices or assessments, even though the debt itself should not be taxed.

3. Plan For Timing And Tax Brackets

The timing of a debt settlement can influence the size of the tax bill that follows.

- Forgiven debt is included in income for the tax year in which the cancellation occurs.

- A large amount of canceled debt can increase total taxable income and push a taxpayer into a higher tax bracket.

- Resolving multiple settlements in the same year can significantly increase the overall tax owed.

- Settling debt in a year with lower overall income may reduce the tax rate applied.

- Spreading settlements across different tax years can prevent large income spikes.

- Coordinating settlements with other deductions or losses may soften the tax impact.

- Insolvency must be measured immediately before the debt is canceled.

- Settling debt after finances improve may eliminate eligibility for insolvency-based exclusions.

- Poor timing can result in taxes being owed on forgiven debt that could have been excluded earlier.

Timing should be used as a planning tool, not a substitute for legal exclusions. When coordinated correctly, it can reduce the size of a tax bill. When handled incorrectly, it can increase tax exposure.

4. Credit Counseling

Credit counseling is an alternative to debt settlement that can help borrowers manage debt without triggering tax consequences, because it does not involve forgiving or canceling any portion of the debt.

- Credit counseling focuses on repayment and debt management rather than debt forgiveness.

- Counselors work with creditors to negotiate lower interest rates, reduced fees, or structured repayment plans.

- Since the debt is repaid instead of canceled, no taxable income is created.

- No portion of the debt is forgiven or discharged.

- There is no cancellation of debt income to report.

- Creditors typically do not issue tax reporting forms related to debt cancellation.

- You are able to repay the full balance over time with adjusted terms.

- Avoiding tax exposure is a priority.

- You want to resolve debt without settlement or bankruptcy.

- The total amount owed is not reduced.

- Monthly payments may continue for several years.

- It may not be suitable for severe financial hardship or immediate collection threats.

5. Debt Consolidation Or Refinance Loan

Debt consolidation and refinancing are options that can simplify repayment and avoid tax consequences because they do not involve canceling or forgiving debt. Instead, existing balances are replaced with a new loan, often with different terms.

- Debt consolidation combines multiple debts into a single loan with one monthly payment.

- Refinancing replaces an existing debt with a new loan, often at a lower interest rate or with extended terms.

- Because the original debt is not forgiven, no taxable income is created.

- The debt is replaced, not canceled.

- There is no discharge of debt under IRS rules.

- No cancellation of debt income needs to be reported.

- You have sufficient credit to qualify for a new loan.

- Your income supports ongoing monthly payments.

- You want to avoid the tax exposure associated with debt settlement.

- The total amount owed usually remains the same.

- Interest paid over time may increase overall cost.

- These options may not be available to borrowers with poor credit or significant financial distress.

Debt decisions can carry serious tax consequences when handled incorrectly. J. David Tax Law has helped clients resolve over $800 million in tax debt, giving the firm deep insight into how debt relief and IRS rules intersect. Call at (888) 342-9436 & let a qualified tax attorney help you understand your options.

Reporting Settled Debt To The IRS

After a debt is settled, the IRS tracks forgiven debt through third party reporting, and taxpayers are required to reflect that information accurately on their tax returns. This section explains how the IRS identifies settled debt and what is required to avoid reporting errors.

- Creditors report forgiven debt to the IRS using Form 1099 C when $600 or more is canceled

- The same form is sent to the taxpayer and matched against the filed tax return

- Receiving a Form 1099 C does not automatically mean the debt is taxable

- The forgiven amount must still be reported or excluded correctly on the return

- Failure to address the form often results in automated IRS notices or assessments

- Errors on Form 1099 C should be corrected by the creditor before filing

This reporting process is why exclusions such as insolvency or bankruptcy must be claimed properly. When reporting is done correctly, the IRS recognizes the exclusion. When it is not, the IRS assumes the forgiven debt is taxable.

Risks Of Ignoring Taxes On Settled Debt

Ignoring the tax side of a debt settlement can turn a resolved debt into a new IRS problem. Even when the underlying settlement is legitimate, failing to report forgiven debt correctly can trigger additional tax, penalties, interest, and escalating enforcement.

If the IRS determines that forgiven debt should have been included in income and it was not reported or excluded properly, it may assess additional tax and add penalties and interest.

Common consequences include:

- Interest accruing on unpaid tax until the balance is paid

- Failure to pay penalties when tax is owed and not paid on time

- Accuracy related penalties when income is understated

- Additional charges and enforcement actions if the balance remains unpaid

Even when a taxpayer qualifies for an exclusion, penalties and interest can still become an issue if the return is filed incorrectly and the IRS later adjusts the tax due. Not sure how much you owe? Use our free penalty & interest calculator to calculate your debt amount.

Most taxpayers will face civil consequences first, including IRS notices and assessments. But continued non reporting or ignoring IRS correspondence can escalate.

Potential outcomes include:

- IRS deficiency notices requiring a response and documentation

- Collection actions if a balance is assessed and remains unpaid

- Tax liens or levies in more serious cases

- Increased exposure if the IRS believes non reporting was intentional

The safest approach is to treat forgiven debt as a reporting issue that must be handled correctly, even when you believe an exclusion applies. Proper reporting and documentation are what prevent the IRS from treating the forgiven amount as taxable income.

Conclusion

Debt settlement can reduce what you owe, but it does not automatically eliminate the tax consequences that follow. In most cases, forgiven debt is treated as taxable income unless you qualify for an IRS exclusion such as insolvency or bankruptcy and report the settlement correctly using the required forms. Understanding how debt settlement tax implications work, reviewing Form 1099-C for accuracy, and filing IRS Form 982 when applicable are critical steps in avoiding unnecessary taxes, penalties, and interest. When handled properly, debt settlement can provide real financial relief without creating new IRS problems.

Frequently Asked Questions

You can avoid paying taxes on a 1099-C only if you qualify for an IRS exclusion, most commonly insolvency or bankruptcy, and report it correctly using IRS Form 982. Receiving a 1099-C does not automatically mean you owe taxes, but it must be addressed properly on your tax return.

The tax owed on canceled debt depends on how much was forgiven and your overall income for the year. If no exclusion applies, the forgiven amount is added to your taxable income and taxed at your applicable rate, which may also affect credits or deductions.

A 1099-C can significantly increase your taxable income if it is not excluded, potentially pushing you into a higher tax bracket or reducing income-based credits. The impact depends on the amount forgiven and whether the debt qualifies for an IRS exclusion.

Credit card debt by itself does not affect your tax return. However, if part of your credit card debt is forgiven or settled, the forgiven amount may be treated as taxable income unless you qualify for an IRS exclusion.

Debt consolidation generally does not affect your taxes because the debt is not forgiven, only replaced with a new loan. Since there is no cancellation of debt, consolidation does not create taxable income.

The IRS does not have a fixed settlement amount. Through an Offer in Compromise, the IRS may settle tax debt for less than the full balance if you can prove you cannot pay the full amount within the statute of limitations, based on your income, assets, expenses, and ability to pay. You can explore all available tax debt resolution options here.