Yes, it’s possible to get a mortgage if you owe back taxes — but only if your debt is under control.

Mortgage lenders don’t automatically reject applicants who owe the IRS, but they do look for proof that you’re resolving the issue through a formal payment plan or settlement agreement.

If your taxes have led to a federal tax lien, it becomes much harder to qualify, since a lien gives the government a legal claim against your property. The key is understanding the difference between tax debt and a tax lien, and taking steps to address either before applying for a home loan.

This guide explains how back taxes affect mortgage approval, how lenders verify IRS debt, and what legal solutions, like payment plans or lien withdrawal, can help you move forward toward homeownership.

Key Takeaways

You can buy a home even if you owe taxes, but your debt must be under an active IRS or state payment plan.

A federal or state tax lien can delay or block approval until it’s released, withdrawn, or subordinated.

FHA and VA loans allow more flexibility for borrowers with verified payment plans, while conventional loans usually require full resolution.

Lenders confirm your status through IRS transcripts, Form 4506-T, and public lien records.

Working with a tax attorney helps you resolve debt quickly and improve your mortgage eligibility.

Identifying the Issue: Tax Lien or Tax Debt?

Before applying for a mortgage, it’s important to understand whether you simply owe back taxes or if a federal tax lien has been filed against you. These two situations may sound similar, but they affect your ability to buy a home in very different ways.

Tax Debt

Tax debt means you owe money to the IRS or state but haven’t yet entered or completed a resolution. While it can raise concerns with lenders, it doesn’t automatically block mortgage approval — especially if you’ve set up an IRS payment plan or are negotiating an Offer in Compromise.

Tax Lien

A tax lien is far more serious. Once the IRS files a lien, it becomes a public record and gives the government a legal claim to your property. Lenders see this as a direct risk to their investment and often won’t move forward until the lien is withdrawn, paid, or subordinated.

If you’re unsure which situation applies to you, our tax lien attorney can review your IRS account, verify lien status, and help you take the right legal steps to restore mortgage eligibility.

The IRS is Forgiving Millions Each Day. You Could Be Next.

How Tax Debt Affects Mortgage Approval

Having tax debt doesn’t automatically stop you from getting a mortgage, but it can slow down or limit your options. Here’s how lenders evaluate your situation:

Debt-to-Income Ratio (DTI): Back taxes increase your total debt load, which can push your DTI beyond lender limits and reduce borrowing power.

IRS Payment Plan Status: Most lenders require proof of an active payment agreement and at least three consecutive on-time payments before approval.

Documentation Requirements: You’ll need to provide a copy of your IRS agreement, payment history, and sometimes your latest IRS transcript for verification.

Loan Type Differences: FHA and VA loans are generally more flexible with approved IRS payment plans, while conventional loans often have stricter debt conditions.

Unresolved Debt Risks: If your taxes are in collections or the IRS has issued an intent to file a lien, lenders may pause your application until the issue is settled.

How Does a Federal Tax Lien Affect Buying a House?

A federal tax lien is one of the biggest obstacles to mortgage approval because it gives the IRS a legal claim to your property. Once a lien is filed, lenders see your assets as encumbered — meaning they could be seized or prioritized by the government before the bank.

Here’s how a lien can affect your ability to buy a home:

Mortgage Denial Risk: Most lenders automatically deny applications if an active federal tax lien appears on your credit or public record.

Title Issues: A lien attaches to all your current and future property, making it difficult to transfer or secure clear ownership during a home purchase.

Credit Impact: Although newer credit reports don’t always display tax liens, many lenders still run public record checks that reveal them.

Higher Loan Requirements: Even if approval is possible, expect stricter conditions — such as higher down payments or lower borrowing limits.

Resolution Needed Before Closing: Lenders typically require the lien to be paid, released, or subordinated before the mortgage can close.

Working with a tax lien attorney can help you request lien withdrawal, subordination, or release, depending on your financial and legal standing — all of which can reopen your path to homeownership.

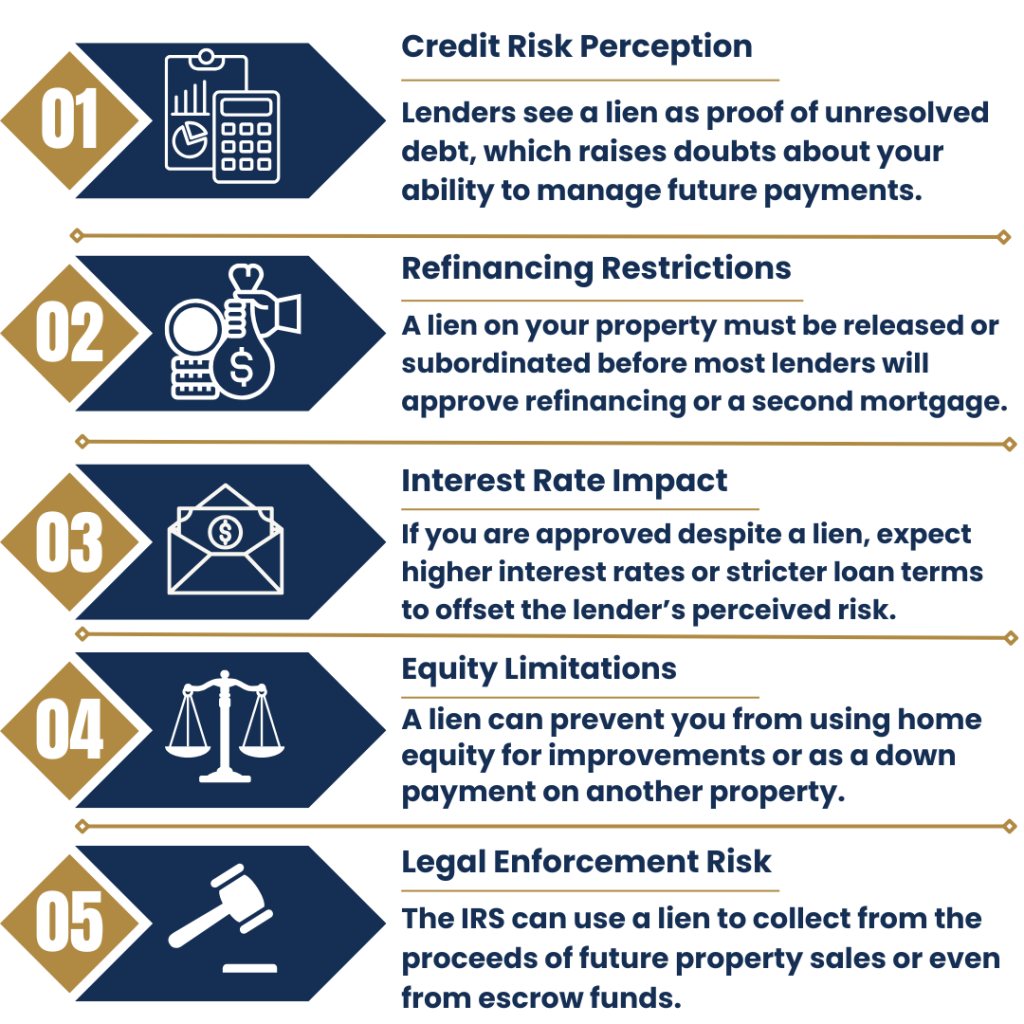

Other Ways a Tax Lien Affects Buying a House

Even if you’re not currently trying to sell your home, an existing federal tax lien can still cause issues when you apply for a new mortgage or refinance. Beyond blocking approval, it can create lasting financial and legal challenges.

Here’s how a lien can affect your ability to buy or finance a home:

How Federal Tax Liens Affect Selling Your Home?

A federal tax lien doesn’t just affect buying — it can also complicate selling your home. Because the IRS has a legal claim to your property, you can’t transfer ownership freely until that claim is resolved.

Here’s how a lien impacts the selling process:

Title Clearance Delays: The lien must be cleared before the title can transfer. Title companies and buyers won’t proceed until the lien is resolved or released.

Reduced Sale Proceeds: Any money from the sale may first go toward paying your tax debt, reducing what you receive at closing.

Limited Buyer Interest: Buyers and lenders are cautious about homes with unresolved liens, which can shrink your potential buyer pool.

Closing Delays: The IRS must issue a Certificate of Release or lien subordination before the sale can be finalized — a process that can take weeks if not managed by a tax professional.

Legal Negotiation Options: A tax attorney can help you request a lien discharge for the property or negotiate partial payment terms to allow the sale to close.

How Do Lenders Know You Owe Taxes?

When you apply for a mortgage, lenders verify more than your credit score — they also review your tax history to ensure you’re not carrying unresolved IRS or state tax debt. Even if a lien doesn’t appear on your credit report, there are several ways lenders confirm whether you owe taxes and whether your account is in good standing.

Tax Returns Review

IRS Form 4506-T (Transcript Request)

Most lenders require you to sign IRS Form 4506-T, which allows them to access your tax transcript directly from the IRS. This document shows your official filing status, reported income, and any outstanding tax balances or payment agreements — providing lenders verified evidence of your tax standing.

Public Records Search for Tax Liens

Disclosure Requirements and Loan Fraud Warning

Proof of IRS Payment Plans

Can You Get a Mortgage if You Have IRS Tax Debt?

Yes, you can still qualify for a mortgage if you owe the IRS — but only if your tax debt is being properly managed. Lenders understand that owing back taxes isn’t uncommon, but they need assurance that you’ve taken formal, verifiable steps to address it. The difference between approval and denial often comes down to documentation, payment consistency, and the absence of active liens.

Here’s how most lenders evaluate your eligibility when you have IRS tax debt:

Active IRS Payment Plan in Place

Lenders view a formal Installment Agreement as a positive sign. It shows you’re cooperating with the IRS and have structured your repayment. The key is that your account must be current — no missed payments and no pending enforcement actions.

Three Months of On-Time Payments

Supporting IRS Documentation

No Active Tax Liens

Clean Financial Standing

The Effect of Owing Taxes on Different Home Loan Types

Owing taxes doesn’t affect all home loans equally. Each loan type, FHA, VA, and Conventional, has different requirements for borrowers with IRS or state tax debt. Here’s a quick breakdown:

| Loan Type | Impact of Tax Debt | What Helps You Qualify |

|---|---|---|

| FHA Loan | Flexible, allows IRS debt if managed properly. | Active IRS payment plan and 3+ months of on-time payments. |

| VA Loan | Moderate, IRS debt must be in good standing. | No active lien and proof of current IRS repayment. |

| Conventional Loan | Strict, most lenders deny if any debt or lien exists. | Full tax resolution or completed Offer in Compromise. |

When to Contact a Tax Attorney Before Applying for a Mortgage

Buying a home when you owe back taxes is possible, but only when your IRS or state debt is resolved, managed, or legally protected. Whether you need to remove a tax lien, negotiate an Offer in Compromise, or set up a compliant IRS payment plan, acting before you apply for a mortgage can make the difference between approval and denial.

At J. David Tax Law, our experienced tax attorneys help clients nationwide restore mortgage eligibility by resolving tax debt quickly and legally — often within days. If you’re planning to buy a home but have outstanding tax issues, schedule a free consultation today to discuss your options for settlement, lien removal, or payment relief.

Other Related Resources:

How to Clear Tax Liens and Protect Your Finances